Rising Interest Rates in Commercial Underwriting

By: Kenneth Bennett, CPA

In the previous twelve month period, the Federal Open Market Committee (FOMC) has increased short-term interest rate targets by 50 basis points:

In addition to slower growth rates in, or even declining, commercial real estate values, future interest rate rises could have measurable effects on repayment ability. Borrowers with variable rate loans face increased debt service or, in the case of a fixed rate loan, the potential inability to refinance at the end of the loan term. Some substantial increases have historically happened in relatively short periods of time.

In a sample scenario, assume a $1 million loan, amortized over a 20 year period, secured by income-producing commercial real estate with non-escalating long-term leases and a 9% debt yield. A loan originated in November 2015 with an interest rate variable at WSJ Prime (3.25% at the time). An original debt service coverage ratio (DSCR) of 1.32x would now have decreased to 1.26x of January 2016 – assuming daily or monthly interest rate adjustments (Prime currently at 3.75%).

- December 15, 2016 – 0.50-0.75%

- December 17, 2015 – 0.25-0.50%

- Prior Target – 0.00-0.25%

In addition to slower growth rates in, or even declining, commercial real estate values, future interest rate rises could have measurable effects on repayment ability. Borrowers with variable rate loans face increased debt service or, in the case of a fixed rate loan, the potential inability to refinance at the end of the loan term. Some substantial increases have historically happened in relatively short periods of time.

In a sample scenario, assume a $1 million loan, amortized over a 20 year period, secured by income-producing commercial real estate with non-escalating long-term leases and a 9% debt yield. A loan originated in November 2015 with an interest rate variable at WSJ Prime (3.25% at the time). An original debt service coverage ratio (DSCR) of 1.32x would now have decreased to 1.26x of January 2016 – assuming daily or monthly interest rate adjustments (Prime currently at 3.75%).

An increase of 350 basis points from the interest rate at origination results in a DSCR decrease to less than 1.00x.

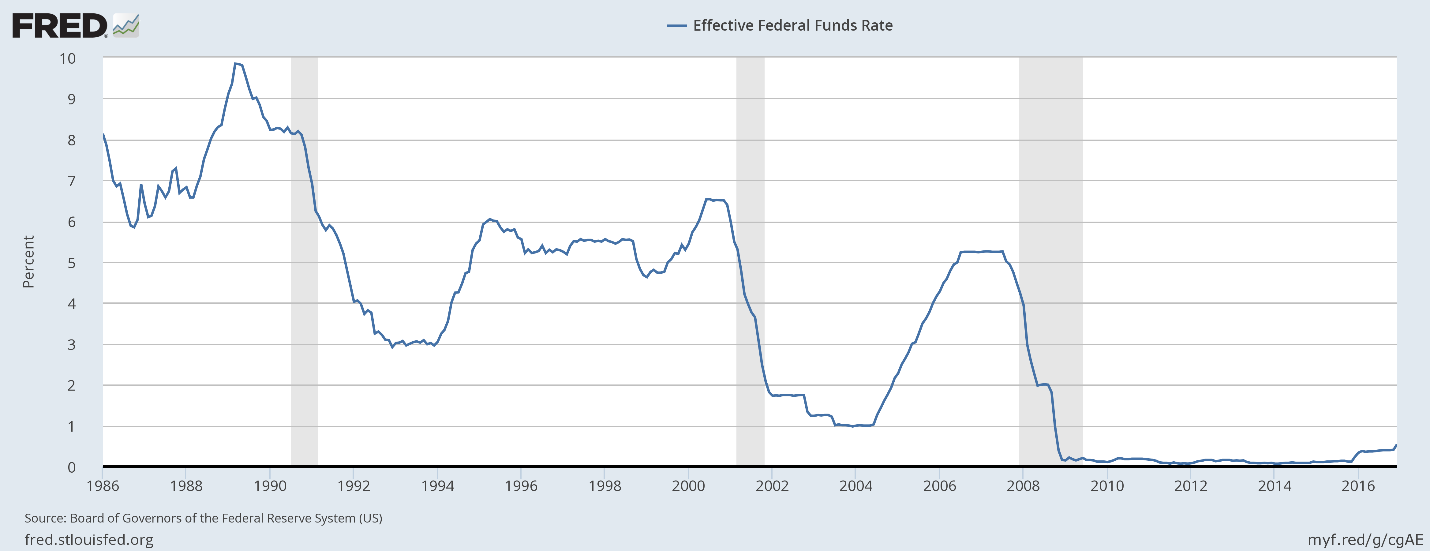

Considering recent history – the past decade or so – a 350 basis point rise in interest rates may seem extreme; however, consider historic rates and rate increases in the Federal Funds Rate – and in turn, the Prime and LIBO Rates:

Considering recent history – the past decade or so – a 350 basis point rise in interest rates may seem extreme; however, consider historic rates and rate increases in the Federal Funds Rate – and in turn, the Prime and LIBO Rates:

Over a fairly recent three year period preceding the great recession, target Federal Funds Rate rose approximately 425 basis points:

Also note that in a single year (1994), interest rates rose approximately 250 basis points – from 3.00% to 5.50%.

Prudent and conservative underwriting should consider the effects of future interest rate changes on borrower repayment capacity. Income producing property with a strong long-term tenant and lease payments resulting in a 1.15x DSCR may need to be viewed with additional caution. Modern underwriting includes testing at various interest rate levels or “shocking” the interest rate at a very increased level to assess repayment capacity.

- 2004 – From 1.00% to 2.25%

- 2005 – From 2.25% to 4.25%

- 2006 – From 4.25% to 5.25%

Also note that in a single year (1994), interest rates rose approximately 250 basis points – from 3.00% to 5.50%.

Prudent and conservative underwriting should consider the effects of future interest rate changes on borrower repayment capacity. Income producing property with a strong long-term tenant and lease payments resulting in a 1.15x DSCR may need to be viewed with additional caution. Modern underwriting includes testing at various interest rate levels or “shocking” the interest rate at a very increased level to assess repayment capacity.